During the first half of this year, about 41,000 battery-electric cars sold in the United States—representing a miniscule .05 percent of all new vehicles purchased nationwide. Electric vehicles remain an aspirational, rather than a practical, buy for many Americans, largely because the lithium-ion (li-ion)battery pack used in nearly every model adds a significant chunk of change to the MSRP—an average of about $15,000, according to a recent report in Plug-In Cars.

There are, of course, other critical factors that create consumer concern, such as lack of charging infrastructure and range anxiety; however, in this economy, higher pricing can be prohibitive to EV adoption.

In reaction, automakers are offering incentives and price cuts simply to get prospective buyers behind the wheel. Just this month, Ford slashed the cost of its 2014 Focus EV by $4,000, bringing it down to $35,999; and last January, Nissan reduced the sticker price on its new Leaf S series to $28,800—undercutting its previous least expensive Leaf by $6,400, or 18 percent.

PwC Study

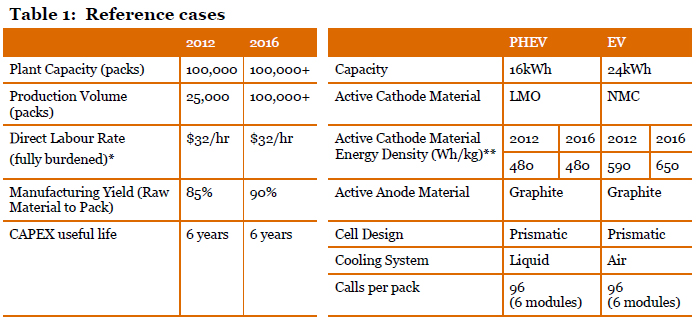

Thus, the fundamental question remains, can battery manufacturers meet the price expectations of the automotive market? PricewaterhouseCoopers (News - Alert) LLP (PwC), a professional services firm based in London, released a “Lithium Ion Battery Cost Study”that looks “slightly into the future,” to those vehicles and programs slated for production in 2016 and beyond. Realizing that the batteries for EVs that are either currently in production or in an OEM’s near-term pipeline already have been sourced, PwC’s analysts looked at the next generation of battery deployments.

PwC interviewed OEMs across several geographies, with a focus on U.S. and European manufacturers, and a mix of volume, luxury and start-up companies. Battery producers also were asked to participate, in order to validate key assumptions about technology and operational cost drivers, and to gain an external perspective on OEM customer requirements. In addition, industry experts provided perspective on where technologies and prices are headed in the next three to five years. Based on the data gathered, the research team conducted a “detailed tear-down of battery costs and associated drivers.”

Chart courtesy of PricewaterhouseCoopers LLP (PwC)

Lower-priced Sales Driven by Scale

The results suggest an achievable battery cost of $425/kWh for the EV reference battery ($10,200/pack) by 2016, and $570/kWh for the PHEV reference battery ($9,120/pack). Indeed, according to the analysts, the industry is well on its target path to reach battery pack costs of $300/kWh by 2020—about half of today’s price.

The research also confirms that the majority of cost reductions in the next five to seven years will be driven by scale and manufacturing process enhancements. Technology advances will contribute a moderate amount during this timeframe, but will play a much bigger role in 2020 and beyond.

In conclusion, PwC states, “Based on our comprehensive analysis, we believe it will be possible for producers to profitably deliver batteries at a target price that will help OEMs improve the cost competitiveness of their vehicles, thereby encouraging consumer adoption and industry scale. However, driving cost out of the value chain and manufacturing operations will not happen automatically; it will require a multi-faceted approach combining operational productivity enhancements with the right product, partnership, manufacturing, supply chain, and footprint strategies going forward.”

Accelerating Advanced Battery Technology

The New York Battery and Energy Storage Technology Consortium (NY-BEST) and DNV KEMA Energy & Sustainability—an energy consultancy and authority in testing, inspection and certification based in Arnhem, Germany—are partnering to build a $23 million Battery and Energy Storage Technology (BEST) Testing and Commercialization Center in Rochester, N.Y.

Under the partnership agreement, DNV KEMA will provide up to $16 million, including the cost of relocating its existing energy storage testing operations from its laboratory facility in Pennsylvania to Rochester. DNV KEMA will operate the new center, after it opens in December of this year.

NY-BEST, a consortium of battery and energy storagecompanies, universities and industry partners, has received $6.9 million in combined funding from the New York State Energy Research and Development Authority (NYSERDA) and Empire State Development Corporation (ESD) toward the creation of the battery and energy storage commercialization center.

The new Test and Commercialization Center will be dedicated to “finding the key missing elements necessary for product commercialization and growth in the energy storage business, including a suite of test, validation and independent certification capabilities to accelerate commercial deployment of energy storage technologies.”

A recent Economic Impact Study commissioned by NY-BEST estimated that the energy storage sector currently employs approximately 3,000 people in New York State and is responsible for more than $600 million in annual global sales. The study found that the sector could grow more than 11,400 new jobs by 2020 and 43,000 new jobs by 2030. The BEST Testing and Commercialization Center will serve as a key catalyst and magnet for attracting and growing the battery and energy storage industry in New York.

Edited by Rachel Ramsey

Internet Telephony Magazine

Click here to read latest issue

Internet Telephony Magazine

Click here to read latest issue CUSTOMER

CUSTOMER  Cloud Computing Magazine

Click here to read latest issue

Cloud Computing Magazine

Click here to read latest issue IoT EVOLUTION MAGAZINE

IoT EVOLUTION MAGAZINE